Announcements

Drinks

Mathias Pleissner

Analyst

Karlo Fuchs

Team leader

Keith Mullin

Press contact

Inflation fuels real house-price declines across Europe

By Mathias Pleissner, Deputy Head, Covered Bonds

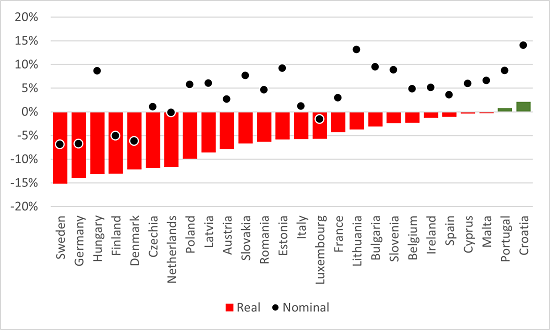

Only seven out of 30 European countries suffered nominal house price reductions over this period. Taking into account the decades of rich property price increases fuelled by ultra-low interest rates, latest developments are tolerable. In nominal terms, European house prices are on average back at 2022 levels. Only Finland has seen house prices fall to 2020 levels.

Average growth across the euro area was still a positive 4.1%, according to latest data released by Eurostat. The picture does not change much if extended to Europe including Norway, UK and Switzerland.

House prices across Europe reveal how much diversity there is in inflation in Europe: latest euro area inflation for the second quarter ranged from 1.6% to 11.3%. Viewing house-price developments in inflation-adjusted terms paints a different picture. Inflation in Europe has been well above nominal house-price growth (if any) so there was a real weighted average decline of 8.4% in the year to end Q1 2023. This can be seen most clearly in countries that have suffered both declines in nominal house prices and high inflation.

Annual house price growth to Q1 2023: real vs nominal

Source: Eurostat, Scope Ratings

In real terms, we are back on average to 2020 levels, before the economic effects of the pandemic boosted house prices. For Sweden, though, house prices in Q1 2023 had fallen to 2016 levels. Germany fell back to 2019 levels. The most severe impacts are Finland, where deflated house prices are at levels not seen for more than 20 years.

While deflated house prices reveal real value loss, they may on the plus side help to push some European mortgage markets into recovery mode more quickly than expected. And if employees can benefit from inflationary wage increases, even marginally, low real-term house prices may help to boost affordability more quickly than expected, despite higher mortgage rates.

Make sure you stay up to date with Scope’s ratings and research by signing up to our newsletters across credit, ESG and funds. Click here to register.

Mathias Pleissner

Analyst

Karlo Fuchs

Team leader

Keith Mullin

Press contact