Announcements

Drinks

Alessandro Boratti

Analyst

Marco Troiano

Team leader

Keith Mullin

Press contact

Italian banks: asset quality unfazed by end of Covid moratorium programmes

The largest Italian banks reported solid annual results, emerging stronger from two years of pandemic. In 2021, banks’ return on tangible equity hit levels not seen in years, in some cases above 10%, while capital buffers remained comfortable. For once, asset quality was not in the spotlight as there were no NPL cliff effects following the progressive lifting of support measures for borrowers.

The vast majority of Italian moratorium programmes expired with the end of the “Cura Italia” decree in December. As of January 2022, the few positions outstanding were down to the banks’ own measures and those put in place by the ABI (the Italian Banking Association). The performance of loans that had been included in expired moratorium programmes has been surprisingly strong. Default rates were in the range of 1%-2.8%, a very manageable level for Italian lenders.

Our 20 September 2021 report (Italian banks: no cliff effects from expiring payment holidays) stressed default assumptions for Italian banks and showed that even under stressed default assumptions (up to 20% default rates on outstanding loans under moratorium at the time), the impacts would be moderate both in terms of gross NPL ratios (+101bp) and provisioning needs (+51bp).

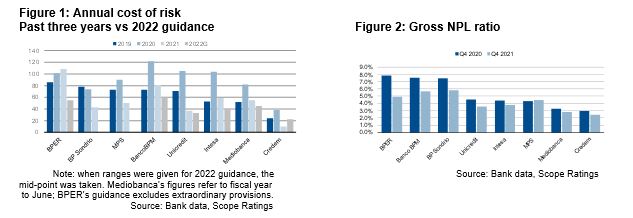

Although banks do foresee a small pick-up in default rates in 2022, they generally guide to cost of risk remaining lower than last year (about 45bp vs an average 55bp in 2021), owing to higher loan volumes and a decline in provisions relating to NPL disposals. See Figure 1

Italian banks’ asset quality improved in 2021; as demonstrated by a decline in average NPL ratios (see Figure 2 above). While inflows of deteriorated positions remained at record lows, banks carried on with disposals (about EUR 30bn at national level). We do not expect this trend to end just yet. Banks are now targeting ever lower NPL ratios to catch up with the EU average of around 2.5%. Intesa is striving become a zero-NPL bank by 2025, keeping NPLs in line with the Nordic peers. Banco BPM, which presented its plan in late 2021, is set to exceed its 2024 NPL target by mid-2022.

The near-term direction of NPL ratios will clearly depend on Italy’s economic performance in 2022. Gross stage 2 ratios remain elevated (13% in December on average for the six largest Italian banks); their quality could deteriorate further if the economic rebound falters.

Scope has subscription ratings on the following Italian banks:

The public rating on Banca Popolare di Sondrio SCpA is available at https://www.scoperatings.com.

Access all Scope rating & research reports on ScopeOne, Scope’s digital marketplace, which includes API solutions such as for Credit Sphere.

Alessandro Boratti

Analyst

Marco Troiano

Team leader

Keith Mullin

Press contact