Announcements

Drinks

Levon Kameryan

Analyst

Dr. Giacomo Barisone

Team leader

Matthew Curtin

Press contact

Russia: tougher sanctions widen disconnect between rouble and economy, increasing retaliation risk

The EU’s proposed new sanctions are likely to inflict further damage on the Russian economy depending on the details of the final agreement, with increasing risk of retaliatory measures from Russia.

To take stock of Russia’s economic fortunes in the third month of its full-scale war in Ukraine, senior analyst Levon Kameryan has looked at the prospects for growth with the sanctions in place, the factors explaining the rouble’s recovery, what impact new EU sanctions might have and what the Russian authorities could do in response. Download the full report

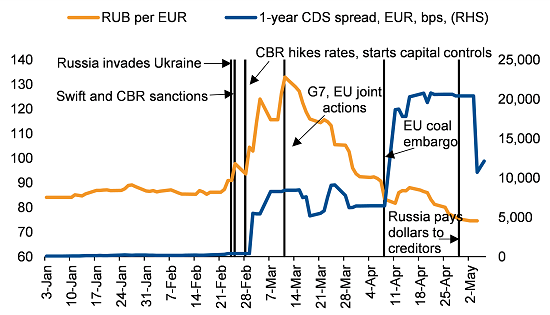

Rouble recovery – is it sustainable?

Two main factors explain the recovery in the rouble. First, high foreign-currency inflows from oil and gas exports – as energy prices have soared – create steady demand for the Russian currency.

Secondly, efforts of the Central Bank of Russia to prevent capital flight through capital controls and higher interest rates, while they are working for now, come at a cost of tighter financial conditions than before sanctions due to elevated credit spreads and low market liquidity, decoupling economic and financial-market activity from the currency’s fortunes.

Russia: rouble exchange rate vs sovereign credit default swap (CDS) spreads

Source: Central Bank of the Russian Federation, Refinitiv Eikon, Scope Ratings

What are Russia’s near- and medium-term growth prospects?

We project Russia’s economic output to contract by at least 10% this year – the steepest decline since 1994 – and stagnate in 2023, knocking the economy back to levels last seen on the eve of the global financial crisis of 2008. To blame are the collapse in private consumption, in investment and in imports as sanctions have taken hold. Russia’s important non-extractive industries – machinery and electrical equipment, computers, cars, pharmaceuticals – are reliant upon imported components. The share of foreign value added exceeds 50% in these industries, with about half coming from the EU, the US, the UK, Canada and Japan, much of which cannot be easily replaced, by imports from China or local alternatives.

In the absence of significant economic restructuring, and assuming sanctions remain in place, we expect Russia’s medium-run growth potential to moderate to 1-1.5% year (from 1.5-2.0%), far below that of most of central and eastern Europe where living standards are far higher.

The EU proposes new sanctions – how tough are they?

In the short term, possibly higher energy prices should help offset the impact of an EU embargo on Russian oil imports.

In the longer term, an EU boycott of Russian oil is likely to imply significant costs for the Russian energy sector and real economy in terms of rouble convertibility, depending on the details of the final agreement, with some EU member states objecting to a full boycott of Russian oil, suggesting the final agreement might be softer than initially expected.

Countermeasures: what steps might the Russian authorities take?

Russia is likely to expand economic retaliation against EU members as it seeks alternative buyers of its energy in Asia, but a complete replacement of the European market is out of reach any time soon due to significant transport and logistical constraints.

Russa’s energy infrastructure is predominantly geared to the west. Immediate expansion of pipeline oil supply to China is limited due to capacity constraints. As for oil supplied by tanker, while China’s independent refiners may be attracted by Russian oil at discounts, state-owned commodity traders may be less so due to concerns around secondary sanctions.

Levon Kameryan

Analyst

Dr. Giacomo Barisone

Team leader

Matthew Curtin

Press contact