Announcements

Drinks

Thomas Gillet

Analyst

Dr. Giacomo Barisone

Team leader

Matthew Curtin

Press contact

Turkey: Erdoğan’s re-election limits prospects for tackling economic challenges, unorthodox policies

By Thomas Gillet, Director, Sovereign Ratings

Now that Erdoğan has extended his rule for another five-year term, the associated policy continuity and challenging economic backdrop will keep pressure on Turkey’s credit ratings (foreign-currency debt rated B-/Negative Outlook) in the near- to medium-term.

The economy is characterised by a below-potential GDP growth rate of 2.7% this year after 5.6% in 2022, a wide current-account deficit, declining international reserves and high inflation (43.4% year-on-year in April).

The prospect of continued expansionary policy making, such as low real central-bank interest rates, is reflected in the lira exchange rate, which has extended losses against the dollar (-8% YTD, 20 TRY/USD), while the 5-year CDS spread has risen sharply to 679 bps.

Capital controls and macroprudential measures, such as limits on cash withdrawals, the deposit protection scheme, and coercive actions on banks’ portfolio allocations, are likely to remain at the core of Turkey’s economic policies.

A partial adjustment of the policy mix is possible, but this would require consistent planning and implementation to be effective. However, President Erdoğan has given little indication of any such U-turn.

Policy continuity risks aggravating already large macroeconomic imbalances

The government’s “lira-isation” scheme has raised resident bank deposits in local currency, although its effectiveness in the long run is unclear. The measure comes at a high cost for public finances, with this cost increasing further in cases of large fluctuations of the lira, making any significant devaluation less likely.

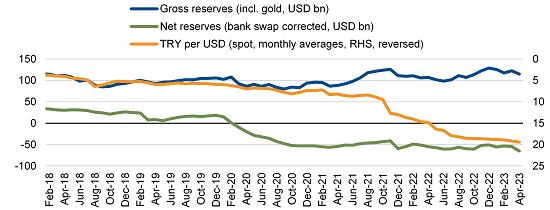

Still, heavily managing the local currency, amid large gross external financing requirements, estimated at USD 230bn in 2023, equivalent to around 25% of GDP, and non-resident capital outflows, requires the central bank to draw on already negative net foreign-exchange reserves once corrected for bank currency swaps, standing at a record-low of negative USD 65.1bn at end-April 2023.

Turkish net reserves are at all-time lows when swap liabilities with banks are deducted

Source: Central Bank of the Republic of Turkey, Scope Ratings

Turkey will need more bilateral and mostly unconditional external support, in the form of direct lending, currency swaps, and energy trade agreements, to partially ease acute pressures on balance of payments and external buffers. However, multilateral assistance would likely remain a last resort as this would entail strict policy conditionality demanded by Western creditors.

Monetary and external imbalances will continue to pressure public finances through measures such as higher salaries and pensions introduced to offset the consequences of the weak lira and a high albeit declining rate of inflation. Such imbalances will also remain a major risk for the Turkish banking sector holding a significant share of government securities, as non-resident holdings of domestic debt dropped to 0.6% by April 2023 from about 20% in early 2018.

Deepening macroeconomic imbalances, resulting from erratic policy making, would inevitably increase the risks of a disorderly adjustment and make any period of policy normalisation more complex to navigate in the longer run. This constrains Turkey’s credit ratings, for which Scope Ratings’ next calendar review date is scheduled on 4 August 2023.

Thomas Gillet

Analyst

Dr. Giacomo Barisone

Team leader

Matthew Curtin

Press contact