Announcements

Drinks

Thomas Faeh

Analyst

Marlen Shokhitbayev

Analyst

Olaf Tölke

Team leader

Matthew Curtin

Press contact

European oil & gas: risks mount for Europe-based companies as Russia-Ukraine conflict intensifies

By Marlen Shokhitbayev, Director, and Thomas Faeh, Executive Director, Corporate Ratings

High benchmark oil prices are good news for the IOC’s exploration and production (E&P) divisions around the globe. Exceptionally high European natural gas prices are most relevant for the region’s direct suppliers such as Equinor ASA and Wintershall Dea AG. Large LNG suppliers such as Shell PLC and TotalEnergies SE also benefit from strong demand. In addition, companies with significant trading operations benefit from the increased volatility in the energy markets.

On the other hand, high energy prices put pressure on refining and petrochemicals margins of the European O&G companies such as Poland’s PKN Orlen SA, Hungary’s MOL PLC and Austria’s OMV AG. However, integrated players should see more upside from E&P than downside from refining and petrochemicals margins.

The catch for the sector is the political component pushing oil prices back above USD 100 a barrel. This is less related to the sanctions imposed on Russia and more to pressure to ostracise the government of President Vladimir Putin because of his decision to wage war on Ukraine.

True, Russia`s invasion of Ukraine has triggered sanctions by US, EU and UK. The most prominent for the energy sector is the halted certification for the Nord Stream 2 gas pipeline, where five European companies (Engie, OMV, Shell, Uniper and Wintershall Dea) provided around half of funds via loans and guarantees.

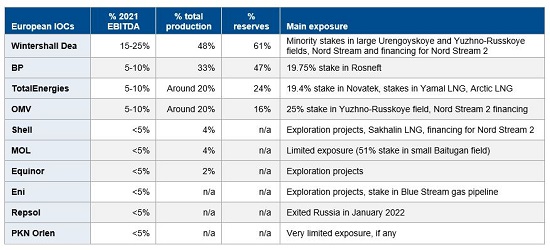

European IOCs’ exposure to Russia’s energy sector

Source: company accounts, Bloomberg, Scope research

Otherwise, the US and EU – which is heavily reliant on Russian energy exports – have spared Russia’s energy sector from the sanctions. The exclusion of selected Russian banks from the Swift international payments system has so far allowed continued trading in Russian oil and gas though private companies have imposed their own sanctions: Credit Suisse and Société Générale have reportedly stopped financing commodity trades from Russia.

Political pressure, however, has mounted on European IOCs to cut their ties with Russia. BP PLC, Equinor and Shell have said they will divest stakes in projects and sell shares in Russian state-controlled oil companies. TotalEnergies and Wintershall Dea have said they will freeze investment.

These decisions are significant. BP’s 20% stake in Russian giant Rosneft accounted for around a third of the company’s hydrocarbon production and around half of its reserves. Others have direct exposure such as Wintershall Dea for which Russia is responsible for around 20% of EBITDA, in addition to a 15.5% stake in Nord Stream and financing for Nord Stream 2.

The effect on credit quality is predominantly on the business risk side. We expect credit metrics to withstand the IOC’s exit from Russia.

Energy prices surge: Brent spot, European gas futures

Source: Bloomberg, Scope Ratings

Other risks could materialise depending on the escalation of the conflict between Russia and the West. These include potential supply disruptions and nationalisation of foreign assets by the Russian state.

While many operators of European refineries and petrochemical plants have diversified sources of crude supplies, Russian oil still accounts for majority of feedstock at PKN Orlen and MOL. Potential supply disruptions from damage to infrastructure or Russian retaliation to sanctions would have consequences for Europe’s energy sector. Industrial corporates in Europe depend on Russian gas for roughly 40% of their energy inputs, so further price increases and disruptions could set back growth. A widening boycott of Russian crude is contributing to rising prices.

An escalation of the conflict would likely send oil & gas prices soaring in the short term, and, if combined with supply disruptions, would stifle growth in Europe, reducing demand in turn as alternative supplies reach the market, translating into lower prices medium term.

Thomas Faeh

Analyst

Marlen Shokhitbayev

Analyst

Olaf Tölke

Team leader

Matthew Curtin

Press contact