Announcements

Drinks

Dennis Shen

Analyst

Dr. Giacomo Barisone

Team leader

Keith Mullin

Press contact

South Africa BB+ ratings constrained by high debt burden, moderate growth potential

By Dennis Shen, Director, Sovereign Ratings

By Dennis Shen, Director, Sovereign Ratings

Longer-run fiscal risk and moderate economic growth potential remain constraints for an investment-grade rating for South Africa – after Scope published BB+ ratings.

South Africa’s fiscal deficit is expected to come in at a better-than-anticipated 4.75% of GDP for FY2022/23 (compared with an earlier government target of 6% of GDP) although we expect this to rise to 5.2% in FY2023/24 and see it climbing during future years because of the rise in interest payments amid higher global rates.

Risks to the budgetary outlook include:

- a renewed recession bringing in lesser tax revenue, and ushering in poorer spending discipline;

- higher wage settlements in view of elevated inflation;

- a further extension or permanent inclusion of the Social Relief of Distress grant – which the government believes could, in lieu of a permanent source of funding, impair sustainability of public finances;

- greater-than-anticipated aid for struggling state-owned enterprises; and

- higher-than-anticipated borrowing costs.

Substantial risks to the national fiscal framework need to be addressed. Current nominal primary expenditure ceilings, which are prudently announced three years in advance, are a credit strength, as is a robust debt and cash management strategy. But higher spending and failure to observe ascribed expenditure ceilings since FY2018/19 undermine faith in the fiscal framework. The adoption of any debt-ceiling rule could complement an existing fiscal architecture and enhance longer-run fiscal sustainability.

Net interest payments are seen rising above 20% of revenue by 2024

We consider net interest payments as a relevant indicator of debt sustainability – reflecting the weight of debt on operational budgetary resources. Net interest payments are expected to average around 18% of government revenue over the next two years, before rising to above 20% by 2024. Sustained deficits have translated to a steady rise of the government debt burden, which is elevated by emerging-market standards.

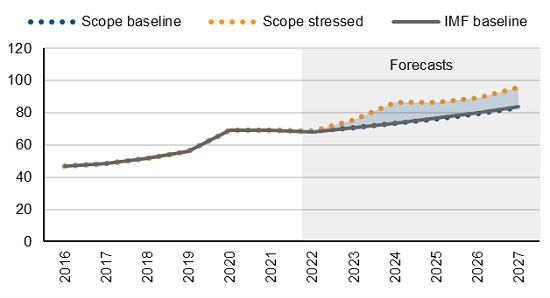

Government debt is seen rising to 73.3% of GDP by 2024, before continuing to increase medium term (Figure 1). Hence, a government expectation in last month’s Medium-Term Budget Policy Statement for a peak of the public-debt ratio at 71.4% by the current fiscal year – two years earlier and nearly four percentage points lesser than previous government estimates – is subject to risk, especially ahead of 2024 general elections.

Figure 1. Debt-to-GDP forecasts, % of GDP

Source: IMF World Economic Outlook (WEO), Scope Ratings forecasts

Low level of sovereign foreign-currency debt mitigates effects of currency losses for debt sustainability

The rand is 7% weaker against dollar since the start of this year, although this has been mainly a dollar-strength phenomenon. The nominal effective exchange rate is largely unchanged. We expect rand will depreciate a further 5% a year against dollar between 2023 and 2027, close to its average rate of annual devaluation from 2012-21.

However, South Africa’s moderate level of sovereign foreign-currency debt mitigates effects from currency losses for debt sustainability, although an elevated participation of non-residents in the domestic debt market represents a further risk. Non-residents held 26.2% of South African domestic debt as of October 2022.

A moderate economic growth trajectory looking ahead

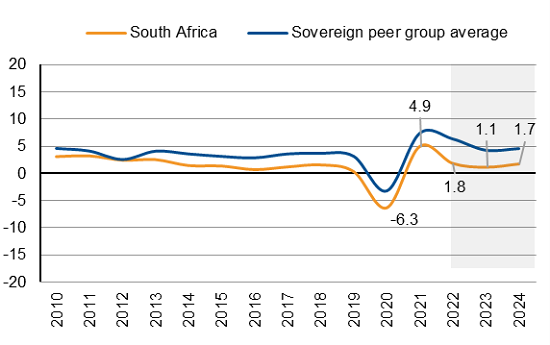

Following a post Covid-19 crisis rebound (4.9% growth in 2021), we see economic growth easing to 1.8% in 2022 before 1.1% for 2023 (Figure 2). The latter is below growth potential of 1.5% a year. We expect 1.7% growth during 2024. A slower economic growth trajectory will prevail despite annual working-age population changes of 1.5% a year anticipated during 2022-27.

Figure 2. Real GDP growth (%)

Source: IMF WEO, Scope Ratings forecast

Growth remains anchored by economic re-openings from Covid-19, but this impetus fades as the international environment has become more challenging. Weak investment expenditure, long-standing energy and infrastructure bottlenecks (especially in rail), as well as labour-market rigidity weigh on growth potential.

Consumer price inflation came in at 7.6% in October, a slight increase from the 7.5% in September but less than the 7.8% print in July. We expect inflation to stay above its 3%-6% target range until Q3 2023 (averaging 7.0% in 2022, 6.3% in 2023 before 4.6% in 2024) and to reach a mid-point of the target range only by mid-2024 – slightly ahead of current central-bank expectations.

Access all Scope rating & research reports on ScopeOne, Scope’s digital marketplace, which includes API solutions for Scope’s credit rating feed, providing institutional clients access to Scope’s growing number of corporate, bank, sovereign and public sector ratings.

Contributing Writer: Keith Mullin

Dennis Shen

Analyst

Dr. Giacomo Barisone

Team leader

Keith Mullin

Press contact