Announcements

Drinks

Dierk Brandenburg

Analyst

Matthew Curtin

Press contact

European companies face tight second-half financing conditions despite less bearish growth outlook

By Dierk Brandenburg, head of credit and ESG research

To be sure, the increase in market interest rates has run out of steam early in the year in the wake of falling headline inflation and sluggish economic growth, shifting investor focus to the longevity of the interest rate cycle.

Money markets already price swift reversal of monetary policy by the end of the year, even though central banks are at pains to convince markets that they will maintain elevated policy rates due to troublesome core inflation running well above target. An inverted yield curve implies that interest rates will remain below their current level in the long-term.

This contrasts with diminishing pessimism on the global economy, with better-than-expected GDP growth in Europe in 2023 – our estimate is for euro area growth of 0.7% - and mounting evidence, such as last week’s payroll report, that the US economy will avoid a hard landing. We estimate the US economy will grow by 1.5% this year.

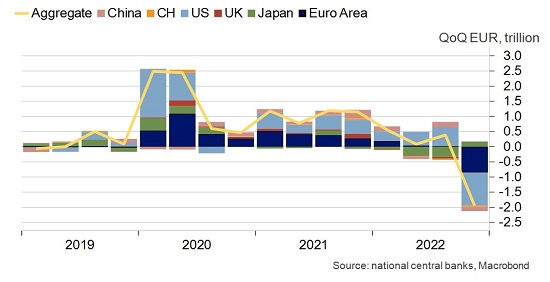

Figure 1: Quantitative tightening is just getting underway

Reversing QE has barely begun in euro area

These developments have led to a strong recovery in financial markets in the New Year, opening an important window for borrowers to refinance maturing debt after a lacklustre 2022, with a rush by European companies to tap debt capital markets in January and February.

However, as far as the normalisation of monetary policy in advanced economies is concerned, the heavy lifting has yet to be done. This will constrict financial conditions through the year. Having cut EUR 2tn of their assets at the end of 2022, global central banks are just getting started on reducing their combined EUR 30tn balance sheet.

The ECB is no exception. The central bank has so far focused on low hanging fruit like removing TLTRO excess liquidity, with quantitative tightening of government bond holdings starting only next month.

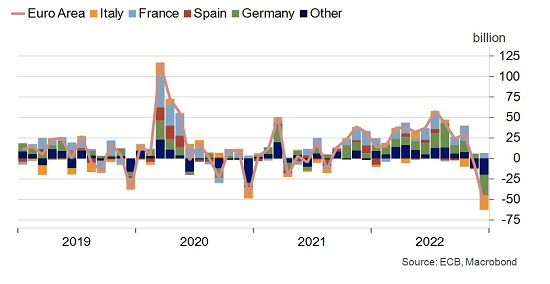

Figure 2: Euro area loans to non-financial corporates fall sharply

Real interest rates to remain higher than in recent past

As much as credit markets have benefited from the recent risk reversal in investor appetite, borrowers will find it harder to access credit compared with the previous decade.

The combination of higher interest rates and falling inflation means the underlying real interest rate will be much higher in future. Long-term real rates have already surged by 200bps and should remain above zero in Europe if growth holds up as expected.

Competition for liquidity will increase as central banks wind down their balance sheets. For the euro area, that results in much higher net issuance by governments in capital markets and falling excess liquidity in the banking system. Already, loans to non-financial corporates are declining and banks are tightening their lending standards.

Figure 3: EU corporates maintain high cash buffers

These effects are yet to be fully reflected in private sector balance sheets. Like banks, large corporates still carry ample liquidity from the pandemic period and benefited from strong earnings in 2022 when they were able to pass on prices to consumers and intermediaries.

However, working capital requirements will remain elevated and with inflation slowing and wages catching up, margins are likely to get squeezed again. Highly levered companies and the unlisted smaller companies will feel the pinch first.

Dierk Brandenburg

Analyst

Matthew Curtin

Press contact